Information for active members.

As part of our fiduciary duty, TTC Pension Plan (TTCPP) provides all active members with a yearly summary of their retirement benefit. By law, this statement must be sent to members by June 30th each year. Your statement will provide you with the amount of your retirement benefit earned up to December 31st of the previous year.

Are you a retired member or deferring your pension?

You will receive a statement every two years. See this article.

Need help understanding the information contained in your annual statement? Let’s take a closer look.

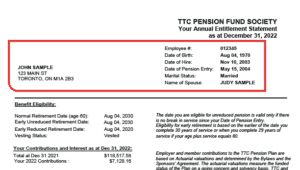

1. Your Personal Information

At the top right on page 1, you will find your basic personal information, including your:

- Name

- Address

- Employee number

- Date of birth

- Date of hire

- Date of pension entry (the date you entered the plan)*

- Marital status

* Note that the date of hire and date of pension entry are not the same. This is due to employees having to complete six months of continuous service before they become a member.

When you receive your statement, take a moment to review this information and let us know if there are any errors or if you have any questions.

2. Benefit Eligibility

In the Benefit Eligibility section, you will see your projected retirement options. These include your Normal Retirement Date, as well as your two early retirement dates:

- Early Unreduced Retirement Date—This is the date you become eligible for early retirement with an unreduced pension.

- Early Reduced Retirement Date—This is the date you become eligible for early retirement with a reduced pension.

To learn more about your early retirement options or how your reduced pension amount is calculated, see Planning for Retirement.

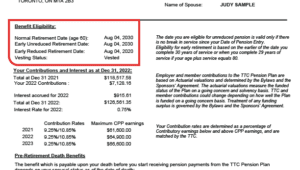

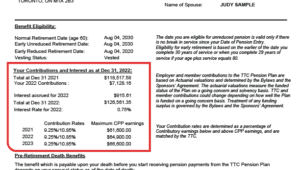

3. Your Contributions

Below the Benefits Eligibility information, you will see the total contributions made by you and your employer, plus interest, as of December 31st of the previous year.

Next, you will see your:

- Contribution Rate—This is the percentage of your earnings each pay that you contribute to the Plan.

- Earnings up to YMPE—This is your year’s maximum pensionable earnings, and is the amount used in the formula to calculate your contributions.

To learn more about how your contributions are calculated, see Plan Features.

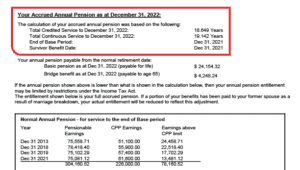

4. Your Accrued Annual Pension

On page 2 of your statement, you will see service information used to calculate your retirement benefit. Note, again, that your Total Credited Service and Total Continuous Service are different.

- Continuous Service—This reflects your total time of service from your date of hire.

- Credited Service—This is the time since you became a plan member. Your total credited service is the figure used in the pension formula.

Both credited and continuous service can be interrupted by breaks in employment such as layoffs, rehires, and certain types of leaves of absence.

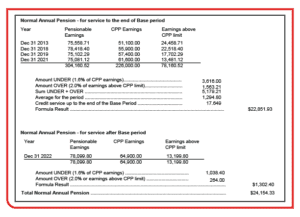

5. Your Normal Annual Pension Calculation

Finally, you will see detailed information about how your pension is calculated.

- Pensionable Earnings—These figures reflect your best four years of earnings, which are used in the pension formula. (Note that your best four years don’t have to be consecutive.)

- Earnings up to YMPE—These are the year’s maximum pensionable earnings in your four best The YMPE is determined annually by the CRA.

The top portion of the box shows the numbers used in the calculation of the Base period pension.

- Base Period—This includes your best four years of pensionable earnings and credited pension service up to December 31st of the base year.

- Average for the Period—This shows you the minimum amount that your unreduced annual pension will grow by each year you continue to work. If a subsequent base period year’s earnings replaces the lowest of your current best four years, this will increase the Average for the period amount of your unreduced annual pension going forward.

- Credited Service up to the end of the Base Period—This shows the total amount of service as the ‘multiplier’ in the base period portion of the formula. The longer you work, and the more years of service are included in the base period at retirement (or termination of employment), the higher your annual pension entitlement will be.

The bottom portion shows the calculation of your non-base period amount.

- Non-Base Period—this includes your pensionable earnings every year after the base period.

The total of your base period amount plus your non-base period amount is your annual pension amount.

To learn more about how your pension is calculated, see Plan Features.

Use your information to estimate your pension

Curious what your pension will be? You can use the information contained in your Annual Statement to generate an estimate of the pension amount you will receive in your retirement. Visit our Pension Estimator to get started and explore different scenarios for your retirement.

Need more help?

We’re always here for you. For help to understand your statement or to update your personal information, contact us.